|

|

| Retirement Planning |

|

| How much do you need to save for retirement? |

We believe that the first � and one of the most pressing � financial questions you need to answer is: How much is enough?

During different stages of retirement, you may experience changes in both your sources of income and in your expenses. You should be prepared to navigate this evolving landscape so that you always have enough.Zenith Integrated, Inc. with our partners leading products go beyond traditional 401(k) and IRAs to help you meet your financial goals. |

| |

| Are you ready to revolutionize your retirement? |

| The Zenith Integrated, Inc. and partners are committed to education and research

that is focused on providing Baby Boomers with information to help them

make informed retirement decisions. |

| |

| Are you prepared to lead the retirement revolutionary? |

| Retirement, as such, is at an end. Its replacement focuses on activity, not rest; on opportunity, not limits; and on beginnings, not endings. It provides the rebirth of your dreams, the reforging of your career, the redesign of your life. However, the ability to realize these changes to their fullest requires a renovation of how income is created and maintained so that as a retiree, if that word still applies, you can transform your life and the world around you. |

| |

| Preparing for the next generation of retirement |

| Zenith Integrated, Inc. and partners wants to help you plan a retirement that defies traditional notions and allows you to chase your ideal of a more carefree lifestyle. Browse this site to learn and be inspired by the stories of others.

Your retirement is an opportunity to pursue your dreams as never before. However, planning has to begin now in order to provide time to determine your financial goals so you can pursue your aspirations.

The following principles provide guidelines for how you can manage your retirement assets to help ensure sufficient income throughout your retirement. |

| |

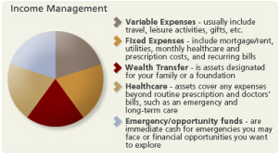

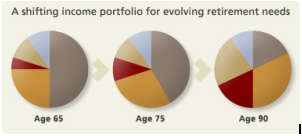

| Revolutionary income management |

This pie chart represents the different uses of your assets during retirement. How much of your portfolio is allocated to each area will be based on your individual needs and goals.

Previous generations of retirees could shift their entire portfolio to income. However, a 30-year retirement requires you to regularly reevaluate |

|

|

| the balance between growth potential, protection, and actual income, to help your assets outlast you. |

| |

| Strategic income allocation |

| Building your income portfolio is the process of selecting the products that will cover your needs and work well together. Five overall strategies exist for filling out your income portfolio, with products generally falling into one of the following categories based on their characteristics. |

| |

|

| |

GROWTH: Provide historically greater returns, though usually with higher risk. These investments help you maintain accumulation potential within your portfolio to potentially outpace inflation. Their more variable nature may make them better suited to variable expenses . However, their growth potential may help maintain the buying power of your income for future fixed expenses.

Examples: Mutual funds , equities.

FIXED: These types of investments provide fixed, stable returns overall. These products and sources are good for fixed expenses . They also may be appropriate tools for more conservative investors seeking wealth transfer.

Examples: Bonds, Social Security, pension payments.

INSURED 1: While these types of products may have a growth or fixed orientation, their primary characteristic is an insurance component that provides some form of insurance protection. The variety of products can cover a variety of income management needs, such as variable expenses, fixed expenses, wealth transfer, and healthcare.

Examples: Annuities , life insurance , long-term care insurance 2.

LIQUID: These products provide easy and quick access to your assets and generally have lower risk and returns. They are traditionally used for emergency funding , whether financial or medical.

Examples: Certificates of deposits, treasury bills, money market funds.

MISCELLANEOUS: The products in this group vary widely and can provide income for fixed expenses , growth potential for variable expenses , or wealth transfer potential.

Examples: Real estate, IRAs, 401(k)s, trusts.

The changes in retirement have intensified the challenges that future retirees will face. Greater freedom in retirement requires greater stability of income, and the control and flexibility to adjust to your evolving needs.

Five most pressing challenges for the retirement revolution:

1. Maintaining your standard of living

2. Rising healthcare costs

3. Making income last your lifetime

4. Changing sources of income

5. Market volatility

For each of the five retirement challenges, several solutions generally exist, allowing you to craft a plan based on your individual goals and profile.

In addition to ensuring that these products and strategies are suitable, you should consider how they work together to provide the best possible mix for your overall portfolio. |

| |

| "As relaxing as being there" |

|

|